The Government of Pakistan held the most recent round of spectrum auction for Next Generation Mobile Services (NGMS) in September 2021. This auction was planned under the Rolling Spectrum Strategy 2020-2023 introduced by the Ministry of Information Technology & Telecom (MoITT) in October 2020. 1 This strategy was formulated based on a Spectrum Master Plan with aim of providing a roadmap for spectrum availability, utilization, and optimization over the next three years with the hope that this visibility will help operators across different telecommunications and media segments plan their operations and investment better. The auction was managed by the Pakistan Telecommunication Authority (PTA), the telecom regulator, even though it is the Frequency Allocation Board (FAB) that is mandated to allocate and manage the radio frequency spectrum for all public, private and defence purposes in the country.

Initially planned for June 2021, the auction was delayed due to cited procedural and approval delays. 2 However, a key plausible driver for the delay was the ambitious perceived inflows by the government through this auction that would help improve the non-tax revenue for the 2021-22 fiscal year and provide some cushion to manage borrowing and other fiscal requirements.

The license term for the auctioned spectrum was to be fifteen years with the following parameters[iii]:

| Band | Availability (paired) | Block Size | Base Price / Block | Base Price / 5 MHz Block |

| 1800 MHz | 12.8 MHz | 5 MHz / 0.2 MHz | USD 31 million | USD 155 million |

| 2100 MHz | 15 MHz | 5 MHz | USD 29 million | USD 145 million |

Other important components of the spectrum auction design included in the Information Memorandum (IM) were a rationalisation plan, Quality of Service (QoS) indicators, and dispute resolution conditions.

Rationalisation Plan

The 1800 MHz band, which provides a preferred spectrum holding for 4G/LTE services and a better mix for urban and rural deployment, has been allocated and used in a manner which does not offer contiguous spectrum blocks to each mobile operator. PTA/FAB have planned to undertake a process • Spectrum auction for Next Generation Mobile Services (NGMS) planned in September 2021 received an underwhelming response from the telecom industry with participation from only one operator and missed both its revenue and spectrum allocation targets. • Boosting access and connectivity with a user-centric approach (affordability and experience) is critical for the adoption of essential applications like digital learning, health and work-fromhome (WFH), as well as supporting Pakistan’s strategic transformation to a digital economy. • Pakistani policymakers need to reimagine spectrum allocation and utilization—from spectrum as a national resource used for short term revenue gains, to spectrum deployed for the achievement of longer term economic goals. 2 for the rationalisation of spectrum in the 1800 MHz band to achieve contiguity, where feasible. This Rationalisation Process may involve a Cellular Mobile Operators’ (CMOs) Existing Spectrum changing from its current position, either up or down in the band. Mobile operators will be required to implement the re-assignment or change in accordance with the Rationalisation Plan within thirty days as per the directives and license conditions.

Quality of Service (QoS) Indicators

The following quality benchmarks were mandated under the spectrum that was to be licensed:

- 3G services: An average download data rate of 512 kbps, which would be increased to 1 Mbps in two years; For upload, throughput to be at least 25% of download throughput.

- 4G services: An average download data rate of 2 Mbps, which would be increased to 4 Mbps in two years, with equal yearly increase; For upload throughput to be at least 25% of download throughput. (A grace period of 6 months in achieving the throughput KPI of 4Mbps will be granted from the second year of the effective date for testing).

Dispute Resolution Conditions

Any disputes raised by licensees will require either:

- Deposit of 50% of the disputed amount in an escrow account opened by PTA and on terms specified by PTA; or

- Furnishing of an unconditional and continuing bank guarantee in favour of PTA equal to 50% of the disputed amount.

Once the dispute is settled, the amount deposited in the escrow account shall accordingly be paid to the Authority or refunded to the Licensee along with bank profit accrued during the period amount was kept in the escrow account. In case of bank guarantee, the same shall accordingly be encashed or returned to the Licensee.

Auction results

Results of the NGMS auction should be a source of disappointment and serious concern for Pakistani policy makers. The auction results undermine the high confidence that should be in place to drive spill over investments by existing mobile operators in the fast evolving and accelerating tech ecosystem in Pakistan. The analysis below summarises results from the auction:

Participation: 25%; one out of four mobile operators participated

Ufone (Pakistan Telecom Mobile Limited – PTML) was the only mobile operator to participate in the auction. This is a positive development, given the unresolved issues from the PTCL privatization where Etisalat acquired management control in 2006.

Spectrum auctioned: 1800 MHz: 70%; 2100 MHz: 0%

Revenue target achievement: 28% of projections

The government had projected the auction to fetch USD 1 billion[i] through the NGMS auction but was only able to generate a revenue of USD 279 million.[ii]

An analysis of spectrum auction rounds held in the past also shows similar failures to meet the targets set. Participation was limited to only one operator in 2016 and 2017, with the spectrum being sold at the base price without competition. The spectrum event in 2014, when the much delayed 3G auction was held, also saw spectrum blocks on offer not being fully purchased by the operators.

Auction results explained

The failure of the NGMS auction to generate the quantum of revenue and the degree of participation that the government sought, must be assessed through two lenses. The first is the set of issues specific to this NGMS auction design and the terms and conditions included in the Information Memorandum (IM). The second is the wider, systemic issues that the telecom industry faces in terms of the operating environment, regulatory landscape and policymaking ecosystem.

NGMS Auction-specific Issues

- Spectrum price and payment conditions: Base pricing of the spectrum was considered too high and does not reflect the market dynamics in terms of market saturation, low Average Revenue Per User (ARPU), dampened growth, and the impacts of a Covid-19 ravaged economy (demand) and the requisite investment in networks to deploy services at scale (supply). In addition, the conditions stipulated that an operator choosing to use a deferred payment option (as opposed to 100% upfront payment) would have their instalments marked up via a peg to LIBOR over the five-year instalment window. Such stipulations likely dampened commercial enthusiasm for participation in the auction.

- License conditions: The Quality of Service (QoS) standards defined in the IM, in the timeframe allocated, seem unreasonably high given the current status of high network utilization and congestion, increasing demand for services and pre-existing spectrum challenges. The QoS requirements mandated in this round also double the existing QoS requirements that operators are required to comply with under the current licensing regime.[iii] While existing average download (18.8 Mbps) and upload (12.9 Mbps) rates in optimal conditions do exceed minimum QoS requirements, offering a network-wide guaranteed experience is a significant challenge for operators.[iv]

- Prohibitive dispute resolution conditions: The dispute resolution conditions require operators to tie up funds irrespective of the process and potential outcomes. In a market with cut-throat competition and value-driving market trends, financial commitments and huge outlays like a spectrum auction payment, deter business interest—especially in light of adverse past experiences. Channelling investments in the network and operations as opposed to dispute resolution securities is a hard sell for investors.

- The high cost of 1800 MHz rationalisation: The rationalisation plan for 1800 MHz can be an extensive and costly exercise for operators and a missing guaranteed timeframe by the government and a very short window of time for implementation by mobile operators can be disruptive to regular operations at a high cost.

Systemic issues

- Economic risks

- Exchange rate risk: The sustained and continuing depreciation of the Pakistani Rupee (PKR) (approximately 28% from 2018 to 2021 alone) affects the business case of investing in Pakistan drastically. Investments made in foreign currencies and revenue and profits generated in local currency continue to suffer from a growing delta as the PKR depreciates. Return on investments (old and new) continue to be diluted and face significant risks in terms of realizing returns in a timely and stable manner.

- Inflation: Inflationary pressures especially for food groups translate into lower spending on discretionary services like internet usage and other value-added services thereby shrinking the market and the potential for revenue growth for mobile operators.

- Taxation: Historically, Pakistan has had one of the highest taxation rates on telecom services. The structure of import, income and sales taxes on the sector significantly impact retail pricing for mobile devices, SIM cards and telecom services thereby affecting usage and ARPU. Sales tax in the mobile sector varies across goods and services and across Pakistan, with rates as high as 19.5% in the provinces.[v] In 2021, the Government of Pakistan had announced the withdrawal of twelve withholding taxes for telecom in June 2021, while taxes on mobile phone calls lasting longer than 5 minutes were also announced at a rate of PKR 0.75 per call.[vi] With one of the lowest ARPUs in the region at PKR 240.5[vii], the case for high investment in spectrum, in the face of relatively low corresponding returns, remains weak.

- Regulatory landscape: The two largest operators – Jazz and Telenor – initiated legal proceedings after their license renewal in 2019[viii] citing concerns that the license renewal conditions are contradictory to the license issuance conditions with regards to the high renewal fee. While the renewal process had been challenged, the operators were mandated to payment of 50% of the renewal fees and after a process of two years, the case was dismissed by Islamabad High Court against the operators and the decision has now been challenged in the Supreme Court of Pakistan.[ix] This kind of litigious context for the Government of Pakistan and telco operators is potentially toxic for the wider investment confidence and the increasingly bright prospects in the technology ecosystem.

Strategic Significance and Implications of the NGMS Auction

Spectrum: The Digital Lifeline

Spectrum is the digital lifeline for growing Pakistan’s digital ecosystem. The boost to Pakistan’s digitization journey during Covid-19 and the traction around pivoting to digital business models has resulted in unprecedented growth and adoption of the internet. Internet usage has increased by approximately 125%[x] over the last year. Mobile operators, despite their best efforts, have been unable to ensure an internet experience that can facilitate now inescapable use-cases like online classes, WFH and an array of new and improved entertainment options, amidst the preventive and containment protocols for Covid-19. Recent QoS assessments by the PTA have exposed many underlying issues of quality, especially in rural areas.[xi] These QoS issues are manifested through slow access/speed and inconsistent experience across geographical locations (urban/rural). The primary reason for this deteriorating service quality is the limited spectrum. The fact that the largest operators did not participate in the auction will have serious ramifications in terms of their capacity to grow and serve new digital entrants and/or continue to offer sub-par experience and thereby limiting the potential socioeconomic upside that may be realised by affordable and ubiquitous digital services.

Strategic Interest of Mobile operators and Foreign Investors

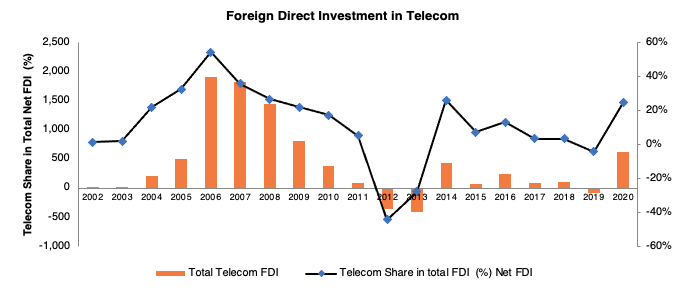

The telecom sector has been a consistent contributor to foreign direct investment (FDI) in Pakistan especially in the early phases of network expansion and growth. Major investment inflows are now restricted to license renewal and spectrum auctions. Over the last decade, the telecom sector has contributed a total of approximately USD 0.8 billion as FDI in Pakistan.

Source: Pakistan Telecommunication Authority

The lack of confidence displayed by the sector in this auction has not only deprived the exchequer of the revenue from spectrum auction but will also constrain associated investments by operators to upgrade and expand networks and services. Limited participation by existing investors also has an important bearing on signalling to new and potential investors actively exploring the digital landscape in Pakistan—this is especially problematic as the government attempts to market the bold reforms that have generated the Special Technology Zones Authority (STZA) and its vital potential role in stirring the latent energy of the tech ecosystem in Pakistan.

Fiscal considerations owing to valuable foreign exchange

At a time when the current account is facing pressure and macroeconomic adjustments to manage economic indicators are on the cards, investment from operators willing to buy spectrum given a conducive environment should have been a welcome source of non-debt contribution to foreign reserves. Leaving an unauctioned spectrum not only limits the upfront foreign exchange that could have been earned, but also impacts both the associated investments in capacity, and the recurring tax revenue that could be generated through consistent growth of the telecom sector directly, and associated sectors indirectly.

Realising the digital opportunity

The recent headlines around start-up funding and record-breaking venture capital interest in Pakistani start-ups are hinged on the opportunity that Pakistan offers. A significant contributor to the opportunity sizing is the growing connectivity and access paradigm whereby internet and smartphone penetrations have reached 54%[i] and 45% respectively.[ii] Sustaining and growing this funding momentum will require a corresponding growth and even more rapid adoption of digital services. The fact that operators may not have the connectivity backbone to enable increased access and adoption at the scale and speed which is required to power the economic and social transformation of Pakistan via “digital” will dampen the growth prospects of local disruptive enterprises that can not only bring in funding but also put Pakistani start-ups on the regional and global map. Fintech, edtech, e-commerce, healthtech and numerous other verticals will rely on an expanded user base and the necessary internet experience to use these services optimally. This will be very hard to do with a backbone that can’t ferry data at speeds commensurate with the needs of the applications and users that will fuel this anticipated growth. Supply side barriers on the connectivity front can be catastrophic for the growth of these services and can have compounded adverse impact on not just economic, but also social indicators.

Course correction

The importance of the spectrum at this critical juncture in Pakistan’s digital journey cannot be overstated. While the government has a complex task to navigate a set of competing priorities and manage endogenous and exogenous factors that impact fiscal and sector decisions, the upside from Pakistan’s transformation to an integrated digital economy and society can contribute massively to addressing some of the perennial challenges. To mitigate the potential fallout from the spectrum auction, the government should:

- Rationalise the base price of the spectrum to adjust for market dynamics in consultation with the industry. The combination of spectrum price, rollout obligations and QoS can be optimized. Doing so requires a dynamic medley of clear objectives, clear priorities and the corresponding spectrum auction design parameters that can be calibrated to achieve the longer-term requirements of a growth-first digital ecosystem. Short-term revenue targets must not be allowed to compromise Pakistan’s longer-term economic potential via its digital positioning.

- Improve associated licensing conditions around payment terms and dispute resolution. These conditions should serve the purpose of improving investor confidence and offering a fair and speedy process that safeguards both the end user (i.e., Pakistani citizens) the government itself, and the private sector enterprises that can fuel economic growth.

- Consider a supplementary spectrum auction to utilize unused spectrum. Unused spectrum at this time will have an opportunity cost associated with the forgone adoption of services like access to digital health, education and financial services in the short term and a dampened trajectory of the digital economy potential in the medium term. Mechanisms to allocate and effectively utilize unused and available spectrum should be explored.

- Pre-empt the next digital opportunity now by building the base for 5G investments in Pakistan. This has an array of components, but they all begin with policy and regulatory vision and clarity. There should be no hesitation by the government to compromise short term revenue targets, if the payoff is the securing of longer-term capacity expansion by telecom operators. The most valuable and impactful economic and social stories of the next stage of Pakistani economic evolution will be in the digital ecosystem—now is the time to build the backbone that will serve that ecosystem. The lessons from the delays in rolling out 3G should inform current and future policy thinking before but it is too late.

Umar Nadeem is the Head of Advisory at Tabadlab. He works at the intersection of evidence, technology and policy with experience in policy analysis, design and management of largescale programmes and digital transformations and has led multi-disciplinary portfolios advising governments and corporations in Asia, Europe and Africa. Umar holds a Master of Public Policy (MPP) from the Blavatnik School of Government, University of Oxford.

Aliza Amin is a Policy Associate at Tabadlab’s Centre for Digital Transformation, where she is responsible for research and analysis of the policy landscape, evolution of digital ecosystems and advisory for transformations. She has been a researcher at Wellesley College and MIT and has worked with non-profit organisations in Pakistan, Morocco and the United States. Aliza graduated from Wellesley College in 2020.

Endnotes

[i] Google & Kantar. (2021, August). Journey to Digital [Webinar]. https://www.youtube.com/watch?v=7mlSvA7MyWo

[ii] Google & Kantar. (2021, August). Journey to Digital [Webinar]. https://www.youtube.com/watch?v=7mlSvA7MyWo

[i] Ali, Kaibe. (2021, May 27). “27.8 MHz spectrum sale to raise over $1bn.” Dawn. https://www.dawn.com/news/1625961

[ii] Karamat, Sonia. (2021, September 16). “Ufone awarded license for 4G services.” Samaa. https://www.samaa.tv/money/2021/09/ufone-awarded-license-for-next-generation-mobile-services/

[iii] Pakistan Telecommunication Authority. (2012, April 12). Cellular Mobile Network Quality of Service (Amendment) Regulations, 2012. https://moitt.gov.pk/SiteImage/Misc/files/cellular_Quality%20of%20Service%20(Amendment)%20Regulations-2012.pdf

[iv] Ministry of IT & Telecom. (2021, January 22). National Broadband Policy 2021: Consultative Draft v1.0. https://moitt.gov.pk/SiteImage/Misc/files/National%20Broadband%20Policy%202021%20Consultation%20Draft(1).pdf

[v] Robinson, J. (2020). Pakistan: progressing towards a fully fledged digital economy. GSMA. https://www.gsma.com/asia-pacific/wp-content/uploads/2020/06/24253-Pakistan-report-updatesLR.pdf

[vi] Geo News. (2021, June 25). ”Budget 2021-22: In final debate session, govt announces adjusted revenue measures, spending plans.” https://www.geo.tv/latest/356869-pakistan-govt-imposes-tax-on-speaking-over-mobile-phone-for-over-5-minutes-shaukat-tarin

[vii] Pakistan Telecommunication Authority. (2020). PTA Annual Report 2020. https://www.pta.gov.pk/assets/media/annual_report_2020_15012021.pdf

[viii] Hussain, Javed. (2019, September 4). “Telenor, Jazz have deposited half of their license renewal fee: PTA.” Dawn. https://www.dawn.com/news/1503499

[ix] Attaa, Aamir. (2021, September). “PTA Wins Licensing Case Against Telenor and Jazz.” ProPakistani. https://propakistani.pk/2021/09/01/pta-wins-licensing-case-against-telenor-and-jazz/

[x] Google & Kantar. (2021, August). Journey to Digital [Webinar]. https://www.youtube.com/watch?v=7mlSvA7MyWo

[xi] Independent Quality of Service Survey in Cities of Pakistan – Second Quarter 2021 https://pta.gov.pk/assets/media/qos_survey_cities_02082021.pdf; https://propakistani.pk/2021/08/03/pta-directs-telcos-to-improve-service-quality-up-to-licensed-standards/;

[i] Ministry of IT & Telecom. (2020, October). Rolling Spectrum Strategy 2020-2023. https://www.pta.gov.pk/assets/media/pak_rolling_spec_strategy_03112020.pdf

[ii] Business Recorder. (2021, June 8). “Spectrum auction: taking time?” https://www.brecorder.com/news/40098390

[iii] Pakistan Telecommunication Authority. (2021, August 5). Information Memorandum: Spectrum Auction for Next Generation Mobile Services (NGMS) in Pakistan 2021. https://www.pta.gov.pk/assets/im_spectrum_auction_pak_05082021.pdf