You can download an e-reader friendly version here.

As various economies around the world begin to ease the containment or suppression measures introduced to counter Covid-19, the threat of new outbreaks looms large. The first phase of policy responses to the economic crisis caused by the virus will now need to evolve, to deal with the potential fallout of a renewed escalation in the numbers of infections and fatalities, and the consequent impact on livelihoods and the wider economy. This First Response argues for the use of monetary and fiscal policy as the instruments with which Pakistan must respond, rather than the relaxing of containment or suppression measures, or easing the “lockdown”.

Throughout February and March, governments all around the world adopted a range of fiscal and monetary measures to deal with the crisis. In Pakistan, an array of monetary and fiscal policy measures was deployed to counter the economic hardship that was anticipated due to the pandemic. Estimates on the degree to which that anticipation has been met may vary, but there is widespread consensus that the “lockdown” and physical distancing measures instituted in response to Covid-19 have come at a very high cost, with a significant drop in economic activity across the country. The Pakistani economy is witnessing a contraction for the first time in nearly seventy years[i].

The First Lockdown: The Cost of Covid-19 Suppression

The Ministry of Planning, Development and Special Initiatives suggests[ii] that the total economic loss under a moderate lockdown is expected to be PKR 1.2 trillion, which is projected to potentially rise to over PKR 2.5 trillion in extreme lockdown scenarios[iii]. Expected GDP growth falls to 0.3% and the economy may actually contract by as much as 1.5% (in effect, a negative GDP growth rate of -1.5%) as the lockdown gets stricter. A strict lockdown will lead to as many as 18.53 million lost jobs. The sectors most likely to be impacted are agriculture, wholesale and retail, manufacturing, and transport.

According to a poll conducted by Gallup recently, 68% of Pakistanis report to have lost their job and 84% report a drop in income.[iv] In short, the “lockdown” imposed by the Pakistani authorities, like in other countries, has proven to be unambiguously costly from an economic standpoint.

Many believe however that the economic costs of the attempts at virus containment or suppression are far less than the costs that may have been incurred by much higher fatality rates, and the wider damage that an unmitigated contagion would have caused.

Containment or suppression efforts in many countries were founded on, among other informants, a recent study conducted by economists at the U.S. Federal Reserve Board and MIT. Using a data set on the U.S. economy during the 1918 Spanish Flu, Correia, Luck, and Verner (2020) find that early and forceful non-pharmaceutical intervention (NPIs) like physical distancing, banning of mass gatherings, and closures of businesses did not worsen the economic contraction. In fact, they find that cities with earlier and more aggressive interventions experienced a relative increase in manufacturing employment, output, and bank assets after the end of the pandemic in 1919. This suggests that the disruption in economic activity is only short-lived, and the positive effects associated with lockdowns in the long-run far outweigh the costs in the short-run. UC Berkley economist Pierre-Olivier Gourinchas posits that aggressive containment measures invariably lead to severe economic recession. In that sense, it may be argued that the economic costs of a lockdown (or “a recession”) is essentially a costly, but necessary public health measure.

In many countries, the debate has evolved into a competing set of views about the potential trade-off between the public health and the economic aspects of the Covid-19. But this dichotomy assumes that a functioning economy can exist concurrent to the emergence of a high fatality pandemic.

Containment or suppression measures in Pakistan that went into force in mid-March are likely to have substantially reduced the rate of the spread of the Covid-19 infection, and thus limit both the rate of fatalities, and the burden on the public healthcare delivery system[v].

The success of early containment measures may help explain the relatively lower rates of infection and fatalities in Pakistan. Being in a better position in comparison to other upper and middle income countries in this regard is cause for doubling down on a successful effort to save lives.

The fundamental logic and evidence upon which the first-wave “lockdowns” were predicated remain solid. A relaxation of restrictions on congregations and social interactions involving large numbers of people is premature.

If the economic impact of a locked down economy is a policy concern, the evidence suggests that it is strong fiscal measures, along with changes to monetary policy that represent a better way to offset economic costs than a premature loosening of restrictions. A second-wave outbreak of COVID-19 would not only be extremely damaging to the economy, but it could potentially overwhelm the country’s already fragile health system leading to the unnecessary loss of human lives, and potential breakdown in public order.

Pakistan’s Fiscal Response to Covid-19

The Government of Pakistan announced an ambitious fiscal stimulus package in March that was aimed at providing much-needed relief to vulnerable consumers and business groups within the country. The USD 8 billion (PKR 1.2 trillion) relief package, which amounts to approximately 2% of Pakistan’s GDP, was meant to ensure that the preventive measures to contain the COVID-19 pandemic do not plunge Pakistan into a self-perpetuating cycle of fiscal pressure and dependence. Of the USD 8 billion fiscal stimulus, cash transfer payments under the Ehsaas Emergency Cash programme worth USD 894 million (PKR 144 billion) are being disbursed to 12 million low-income households. While this is a commendable step, there is still room for further fiscal expansion. Fiscal stimulus packages have been announced by a wide range of middle and upper-income countries across the world. Countries like the United States, Japan, and Iran announced expansive and ambitious stimulus packages worth 10% to 20% of each country’s respective GDP. Not surprisingly, middle and lower middle-income countries like Vietnam, Pakistan, and India, due to their limited resources are ranked at the lower end with fiscal stimuli as low as 1% of GDP.

While a fiscal expansion worth 10% of Pakistan’s economy might be unrealistic, middle and lower middle income countries like Thailand and Indonesia have shown that there is room for further expansions. To be able to shield the poorest and most vulnerable from the economic impact of a lockdown for a prolonged duration, the government will have to take steps to safeguard and guarantee that households have the basic income (especially in terms of food security) required to survive the downturn. This would involve additional cash transfer payments. The motivation for further fiscal expansion is deeply rooted in the macroeconomic literature on business cycles. Research indicates that the impact of a fiscal expansion on the country’s economy tends to be amplified during a contraction or recession, as opposed to when the economy is growing.[vi] If Pakistan is in the midst of a recession, cash transfers and other fiscal measures may have an outsized positive impact on the macroeconomy. Is Pakistan’s economy in recession? If so, how long has it been in this recession?

Estimating Recession Dates for Pakistan’s Economy

Plenty of indicators can help explain the state of an economy, i.e. recession or expansion. Instead of relying on traditional economic measures to characterize a recession, more sophisticated analyses of actual economic data can be used to define periods of economic downturn. Estimating recession dates for Pakistan are crucial to assess the appropriateness of fiscal measures to stimulate growth.

The textbook definition of a recession (a period of diminished economic activity) is often vague and abstract as many approaches can be used to define a recession. Measures like unemployment rate and capacity utilization have been used in various influential studies[vii]. Convention dictates that an economy is considered to be in a recession if it has a negative growth rate for two consecutive quarters[viii]. However, there are several instances when economies across the world despite having positive GDP growth rates were characterized as recessions. The issue in Pakistan’s case is that GDP data is not available by quarter (only annually) limiting the potential to apply the conventional definition of a recession.

Based on studies conducted by Auerbach and Gorodnichenko (2012, 2013) data at high frequency is required to construct recession dates. One way to address this issue for Pakistan is to use an exponential transition function to estimate recession probabilities using the quarterly industrial production index—since this is the only measure of output available at a quarterly basis. This quarterly data[ix] offers a long enough time series (over a decade) to estimate probabilities.[x]

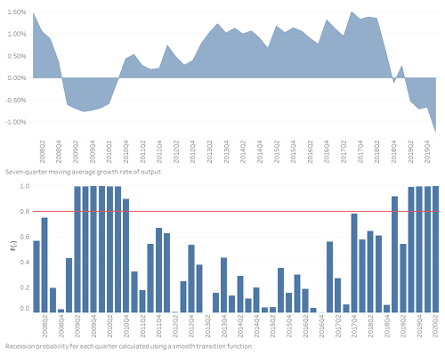

Moving Average of Output

Figure 2 represents the seven-quarter moving average growth rate of industrial production, whereas the lower panel indicates the probability of a recession in each quarter. [xi] Moving averages can be used to smooth out transitory fluctuations in the growth rate of output, and capture the long-term cycles and trends. Based on these results, Pakistan seems to have gone through two periods of sustained diminished economic activity over the last twelve years. The first recession lasted between Quarter 1 of 2009 and Quarter 2 of 2010. This period coincides with the global financial crisis of 2008-2009, during which the Karachi Stock Exchange fell by 64.18%,[xii] and manufacturing output saw a decline of approximately 15%.[xiii] The second period of recession starts during Quarter 2 of 2019 and lasts through the end of the year. Low productivity, a high current account deficit, increasing circular debt, and high unemployment and low growth were hallmarks of this period. This wasn’t help by the fact that Pakistan had an overvalued exchange rate that translated into higher current account deficits because its exports were not competitive.

In short, Pakistan was already in a recession prior to Covid-19 prompted widescale shutdown of the economy to contain the spread of the virus. This implies that two months after the original “lockdown”, Pakistan is likely to have slid further into its ongoing recession.

Probability of Recession Function

In Figure 3, the economy is considered to be in a recession when the value of the plotted transition function is above 0.8 (highlighted with the horizontal line). Based on this definition, there was a recession between Quarter 2 of 2009 and Quarter 4 of 2010. The second period of recession, on the other hand, is consistent with findings using the moving average methodology indicating that Pakistan has been in recession since Quarter 3 of 2019.

Yield Curves

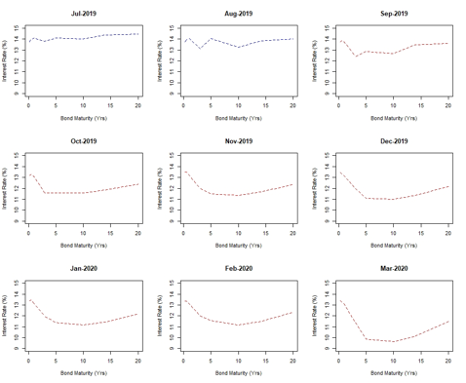

Yield curves plot interest rates of bonds with the same characteristics but different durations (or maturities). The reason why yield curves are given importance globally is that they appear to depict a recession. These are considered to be a good read of people’s future expectations concerning GDP growth, inflation, and unemployment rate. Each inverted yield curve, barring two in the last seventy years, has been preceded by a recession in the US[xiv].

The yield curve essentially illustrates the returns investors get from short and long-term government bonds. Normally yield curves slope upwards, which suggests that as the duration of a bond increases, the return associated with it also goes up. This is because investors demand a higher return for locking their money up for longer. So, if they feel the economy is slowing down, long-term rates end up being lower than short-term rates and the yield curve inverts which is a sign of recession. The reason for this inversion is that as skepticism about the economic growth trajectory increases, investors are likely to buy long-term bonds propping up the price and reducing the interest rates, whereas lower demand for short-term bonds will reduce prices and increase interest rates. Since an abundance of economic agents, ranging from foreign entities to local businesses, invest in the government bond market, everyone is exposed to the same amount of risk. In that sense, yield curves are considered to be a reliable indicator of the market’s aggregate assessment about the future.

Figure 4 represents the yield curves for Pakistan’s economy dating back to August 2019.[xv] A red line indicates the inversion of the yield curve, suggesting long-term rates are lower than short-term rates. In that case, investors have a bleak outlook of the future because the economy is on the brink of a recession. Judging by the inversion of the yield curve, it can be concluded that Pakistan’s economy has been in a recessionary phase from September 2019. The key point to take away from this analysis is that even before COVID-19’s harsh economic consequences on the economy were realized and understood, Pakistan was already in a recession.

The evidence provided by the yield curve inversion, negative moving average growth rate of output, and recession probabilities all point to the confirmation of this hypothesis.

Figure 4: Term Structure of Pakistan Government Bond Rates

Effectiveness of Fiscal Policy During Recessions

Based on the estimation of Pakistan’s yield curves and recession probabilities, Pakistan has been going through a period of economic downturn since September 2019. It is important to establish the recessionary phase of the economy because the impact of a fiscal stimulus will be contingent on the state of the economy. Auerbach and Gorodnichenko (2012, 2013) find large differences in the size of the fiscal multipliers in expansions and recessions. They find that fiscal policy has a higher impact in a recession as opposed to an expansion, with the fiscal multiplier being 1.5 in a recession and 0.5 in an expansion. This suggests that if the government was to increase spending by USD 1, output would increase by USD 1.5 in a recession as opposed to only increasing by USD 0.5 in an expansion. Economists like John Taylor, Oscar Jorda, and Athanasios Tagkalakis also find similar conclusions through various studies.[xvi]

The estimation results suggest that since Pakistan is in the in the midst of a recession, an expansionary fiscal policy is the need of the hour. Intuitively speaking, higher government spending is less likely to crowd out investment during times of recession, which is why it makes sense for the government to announce another fiscal stimulus. Based on a recent policy paper by Nadeem and Zaidi (2020) on Pakistan’s bold income support, the cost of making a one-time PKR 12,000 PKR payment to 12 million households is approximately USD 894 million (PKR 144 billion). A study by University of California Los Angeles[xvii], using data from different countries, forecasts Pakistan is expected to hit the infection peak (number of active cases) on July 18, 2020 after which the curve is likely to flatten. While forecasts like this have to be taken with caution, this does provide a ray of hope. The model, however, assumes that the country continues to exercise reasonably robust containment measures, meaning that the “lockdown” must persist throughout June and July of 2020. Instead of easing restrictions prematurely since May 9, 2020 it should have extended containment measures for at least two months, and complemented this by announcing a second phase of fiscal stimulus package. The focus of this second phase stimulus should be addressing food insecurity among low-income households by expanding the Ehsaas Emergency Cash programme.

Monetary Policy in Pakistan: Setting Policy Rate using the Taylor Rule

In Keynesian terms, the negative supply and demand shock triggered by the coronavirus crisis has led to an economic downturn. Fiscal policy solely might not be sufficient to limit the damage from the pandemic. The severity of this economic crisis suggests that the State Bank of Pakistan has a vital and consequential role to play. The policy instruments at the disposal of the SBP include reducing the policy rate, as well as facilitating businesses through various lending programs.

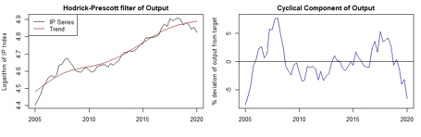

Figure 5: Cyclical and trend component of the Industrial Production of IP Index

While the room afforded through monetary policies to counter adverse economic shocks has been constrained in a number of economies due to already low interest rates, that hasn’t been the case for Pakistan. The State Bank of Pakistan has been aggressive in its conduct of monetary policy so far, with a much-needed 525 basis points cut taking the policy rate from 13.25% to 8% in less than two months. However, based on the Taylor Rule, there is room for further rate cuts. Central banks across the world have used various targeting rules to decide changes to the monetary policy. The Taylor Rule suggests that if actual inflation exceeds the target inflation, then the central bank needs to increase the policy rate. Similarly, a positive output gap is indicative that actual output is higher than potential output, in which case central banks need to engage in a rate hike to prevent the economy from over-heating.[xviii]

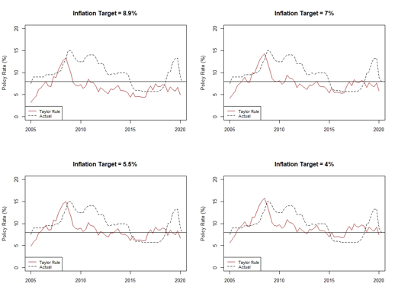

Data on Pakistan’s economy between Quarter 1 of 2005 and Quarter 1 of 2020 is used to construct estimates using the Taylor Rule. The inflation target is chosen based on a recent SBP working paper by Hussain and Rehman (2020), who recommend it to be set at 5.5% with a range of +/- 1.5%. For the purpose of this analysis, the implied policy rate under the Taylor Rule is calculated for multiple inflation targeting scenarios (). It is then plotted alongside the actual rates in Figure 6. The long-run average real interest rate, , is calculated to be 7.76%, and the output gap is estimated using the Hodrick Prescott filter. For graphical illustration of the current policy rate, a horizontal line is drawn at 8% (as this is the current SBP policy rate).

The scenario analysis below[xix] highlights options available to the SBP to adjust the policy rate:

| Inflation Target | Rate Cut (basis points) | New Policy Rate |

| 8.9% | 300 | 5.0% |

| 7.0% | 210 | 5.9% |

| 5.5% | 130 | 6.7% |

| 4.0% | 60 | 7.4% |

The analysis above highlights that the policy rate being maintained by the SBP currently is higher than what the Taylor rule predicts. That being said, an inflation target as low as 4% seems unlikely at this point, given year-on-year inflation for March was recorded to be 10.2%. Keeping interest rates at a higher level to maintain price stability will only further worsen the economic downturn. As a result, it is imperative for the SBP to strike a balance in setting the policy rate, as it tries to achieve the goal of maintaining price stability without hampering the growth.

Figure 6: Monetary Policy Scenarios

Based on the calculations of the policy rate implied by the Taylor Rule and working paper by Hussain and Rehman (2020), an inflation target of 5.5% is more plausible in the short to medium run, and this requires the SBP to reduce rates by 130 basis points to 6.7%. A rate cut at this point will not only reduce the cost of borrowing and encourage investment, but will also be instrumental in generating economic activity.

Proposed Policy Responses for Pakistan’s Second Lockdown

As governments dealt with the first round of the impact of COVID-19, Pakistan took a number of important and urgent steps to combat the risk of plunging the public into a self-perpetuating cycle of fiscal pressure and dependence—a series of infection suppressing and virus containment measures known as the ‘lockdown’ were supplemented with a series of fiscal and monetary steps that helped soften the blow of the lockdown.

As the lockdown has been eased, and human interaction surges in the anticipation of Eid weekend, a surge in infections is expected to both alter the shape of Pakistan’ peak, and speed up reaching Pakistan’s peak infections. This steepening of the curve will need to be met with a second round of containment measures, or a second lockdown. When this is decided, the country will require a new round of fiscal and monetary measures. Given that the country has been in the midst of a recession, even prior to Covid-19’s impact, an expansionary fiscal policy will be necessary. On the monetary side, there is a solid case to be made for the SBP to provide further rate cuts so that it can contain the panic in the stock market and reduce the cost of business—a further rate cut of 130 basis points will be necessary to bring the policy rate to 6.7%, if the target for inflation is 5.5%.

All told, with a second fiscal package worth PKR 480 billion, the outlays of total fiscal stimulus would amount to USD 11 billion (PKR 1.7 trillion), which translates into 3.5% as a share of total GDP. This would raise Pakistan’s outlays to the same level as middle and lower middle income countries, like Vietnam and Indonesia. Moreover, there is motivation for further expansion because the economy is currently going through a period of recession, and this fiscal stimulus will be more effective in boosting the economy in the long run.

| Instrument | Recommendation |

| Fiscal Policy | With the economy currently in the midst of a recession, an expansionary fiscal policy is the need of the hour. Government ought to announce another fiscal stimulus package to the tune of PKR 480 billion (over 1% of GDP) with the following breakdown: |

| 1. Two monthly cash transfer payments to 12 million low-income households worth PKR 288 billion (0.6% of GDP). | |

| 2. Infrastructure bill worth PKR 92 billion (0.18% of GDP) aimed at putting the most vulnerable segment of the labor market, i.e. low-skilled workers, back to work. | |

| 3. Invest PKR 100 billion (0.22% of GDP) in the public health sector to ensure widespread testing and contact tracing. | |

| 4. Engaging in fuel hedging to reduce Pakistan’s exposure to volatile and potentially rising fuel costs as global demand rebounds in the latter part of the year and increased crude oil prices. | |

| 5. Pakistan is expected to have a higher fiscal deficit in the upcoming budget year, with decreasing tax revenues and increased government spending in a bid to tackle COVID-19. In light of this, the government should decide against completely passing on the benefit of low crude oil prices to consumers, and instead use the additional revenue to finance a portion of the fiscal stimulus. | |

| Monetary Policy | Set interest rates subject to inflation targeting in accordance with the Taylor Rule:

For an inflation target of 5.5%, set the policy rate at 6.7%. |

This First Response benefited from inputs from Shafaat Yar Khan, at the University of Rochester, Nazish Afraz, at the Lahore University of Management Sciences, and Uzair Younis, at Dhamiri.

References

Auerbach, Alan J, and Yuriy Gorodnichenko. “Measuring the Output Responses to Fiscal Policy.” American Economic Journal: Economic Policy 4, no. 2 (2012): 1–27. https://doi.org/10.1257/pol.4.2.1.

Auerbach, Alan J, and Yuriy Gorodnichenko. “Output Spillovers from Fiscal Policy.” American Economic Review 103, no. 3 (2013): 141–46. https://doi.org/10.1257/aer.103.3.141.

Benzoni, L., Chyruk, O., & Kelley, D. (2018). Why does the yield-curve slope predict recessions? Chicago Fed Letter. doi:10.21033/cfl-2018-404

Bernanke, Ben and Ilian Mihov. What Does the Bundesbank Target? European Economic Review. 41 (6): 1025–1053. 1997. doi:10.1016/S0014-2921(96)00056-6.

Clarida, Richard; Mark Gertler, and Jordi Galí. Monetary Policy Rules in Practice: Some International Evidence. European Economic Review. 42 (6): 1033–1067. 1998. doi:10.1016/S0014-2921(98)00016-6.

Correia, Sergio, Stephan Luck, and Emil Verner. “Pandemics Depress the Economy, Public Health Interventions Do Not: Evidence from the 1918 Flu.” SSRN Electronic Journal, 2020. https://doi.org/10.2139/ssrn.3561560.

Granger, Clive W. J., and Timo Terasvirta. “Modelling Nonlinear Economic Relationships,” New York: Oxford University Press. 1993.

Hussain, Fayyaz, and Muhammad Rehman . “Estimation of Medium Term Inflation Target for Pakistan.” State Bank of Pakistan Working Paper Series, www.sbp.org.pk/publications/wpapers/2020/wp104.pdf. 2020.

Nadeem, Umar, and Mosharraf Zaidi. “Pakistan’s Bold Covid-19 Income Support: A Portal For Fiscal Transformation?” First Response: Tabadlab. 2020.

Shahid, Ariba. “How Can Pakistan Gain from the Oil Price Crash?” Profit by Pakistan Today, 21 Apr. 2020, profit.pakistantoday.com.pk/2020/04/21/how-can-pakistan-gain-from-the-oil-price-crash/.

Shahid, Ariba. “Refineries given Green Light to Import Crude Oil.” Profit by Pakistan Today, 25 Apr. 2020, profit.pakistantoday.com.pk/2020/04/26/refineries-given-green-light-to-import-crude-oil/.

Taylor, John B, 1993, “Discretion Versus Policy Rules in Practice,” Carnegie-Rochester Conference Series on Public Policy, Vol. 39 (November), pp. 195–214.

Terasvirta, Timo. “Modelling Nonlinearity in U.S. Gross National Product 1889?1987.” Empirical Economics 20, no. 4 (1995): 577–97. https://doi.org/10.1007/bf01206058.

End Notes

[i] https://tribune.com.pk/story/2224516/2-pakistans-economy-contracts-first-time-68-years

[ii] “Coronavirus: Economic impact and relief package”, Edited by Dr Hafiz Pasha AND Shahid Kardar. Business recorder https://www.brecorder.com/2020/03/31/585150/coronavirus-economic-impact-and-relief-package/

[iii] https://tribune.com.pk/story/2189904/2-coronavirus-forecast-render-18-5m-jobless/

[iv] Source: Gallup Pakistan Coronavirus Attitude Tracker Survey 2020, Wave 3.

[v] Nadeem, Umar, “Covid-19 Response Briefing: Locking Out the Virus: Analysis of Pakistan’s Two Month Lockdown”, Tabadlab, May 02, 2020

[vi] Auerbach and Gorodnichenko (2012, 2013) etc.

[vii] Gordon and Krenn (2010, NBER Working Paper) use capacity utilization as a measure of recession.

Reference: Gordon, Robert J. and Robert Krenn, 2010. “The End of the Great Depression: VAR Insight on the Roles of Monetary and Fiscal Policy.” NBER Working paper 16380.

[viii] The commonly accepted definition of a recession in the UK is two or more consecutive quarters (a period of three months) of contraction in national GDP.(https://web.archive.org/web/20121102095705/http://www.hm-treasury.gov.uk/junebudget_glossary.htm)

[ix] Price, Prtoduction and Labour data, IMF Data portal (https://data.imf.org/regular.aspx?key=61545849)

[x] The transition function takes the form . Where is defined as the seven-quarter moving average growth rate of industrial production, and the values of and are chosen based on previous studies that have been used to identify recession periods. Granger and Teravistra (1993), and Auerbach and Gorodnichenko (2012) choose these values by imposing fixed values over and , and then using a grid search to ensure that the is minimized.

[xi] The recession probabilities are constructed following the influential works of Auerbach and Gorondnichenko (2012, 2013), and Terasvirta (1995). Referring to the left column in Figure 4, a negative moving average growth rate of output indicates that the economy is going through a period of contraction and downturn, whereas a positive moving average growth rate of output suggests that the economy is going through an expansionary period.

[xii] The KSE-100 index closed at 15,434 points in April 2008. By March 2009, 64.18% of the points had been wiped out and the index closed at 5,750 points.

[xiii] Output decreased from the 2008 level at USD 25.21 billion to USD 21.39 billion at the end of 2009.

[xiv] Why Does the Yield-Curve Slope Predict Recessions? (https://www.chicagofed.org/publications/chicago-fed-letter/2018/404)

[xv] Yield curves plotted using data on Pakistan Government Bonds downloaded from Investing (www.investing.com).

[xvi] Jorda and Taylor (2016) find that fiscal austerity depresses the economy more when implemented in a slump as opposed to a boom. On the other hand, Tagkalakis (2008) finds that tax cuts are more effective in recessions as opposed to expansions.

[xvii] Source: https://covid19.uclaml.org/

[xviii] Taylor Rule is defined as, Where represents the policy rate, is the long-run average real interest rate, is the average inflation rates from the last four quarters, is the target inflation rate, and is the output gap (difference in actual and potential output) which is estimated using the Hodrick-Prescott Filter. In this equation, Taylor (1993) is followed to set .

[xix] Based on the SBP working paper on the topic titled “Estimation of Medium Term Inflation Target for Pakistan.” (www.sbp.org.pk/publications/wpapers/2020/wp104.pdf).

Dr. Naafey Sardar is an economist interested in Macro and Energy Economics. His ongoing projects study the impact of energy price shocks (large movements in oil and gasoline prices) on the U.S. economy.

Dr. Naafey completed his Ph.D. in Economics from Kansas State University in August 2020 under the supervision of Lance Bachmeier, and he is currently working as a senior research associate and adjunct professor at Texas A&M University in San Antonio.