An e-reader friendly version of this piece can be downloaded here

Since the passage of the 2019-2020 budget, Pakistan’s government finds itself in conflict with associational representatives of the wholesale-retail trade (WRT) sector. The root of this conflict lies in the underlying rationale of the budget itself, which, in turn, is anchored in Pakistan’s latest IMF program.

Briefly put, the stabilization-seeking budget proposes a number of revenue-raising measures in conjunction with extensive documentation of the economy. The documentation aspect works on a relatively simple logic – the government is unable to capture information on the the full extent of the economy, which means a significant volume of activity that should be taxed remains untaxed. As a result, the government remains reliant on a relatively narrow tax-base, which consists largely of taxes on manufacturing and taxes on international trade. Additionally, given the failure of the government to capture economic activity that happens outside these two domains, there is the accompanying failure of capturing actual income, which would lead to higher (and more progressive) direct taxation.

The solution suggested is to better document wholesale-retail trade or WRT activity and ultimately implement the sales tax regime at the point of sale (rather than solely at the point of manufacturing). This is not a unique solution by any stretch. The state’s tax machinery has been attempting to move towards such a General Sales Tax (GST) regime since the 1990s, when the contemporary fiscal structure for taxation was legislated. However, despite attempts, including a particularly wide-ranging one in the shape of army officers deployed through the Survey for Documentation of the National Economy Ordinance 2000, the outcomes have been considerably underwhelming.

What do the numbers tell us?

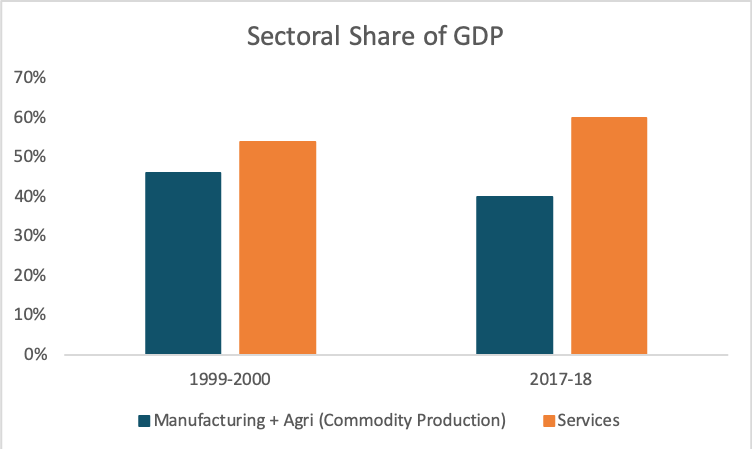

The government’s renewed focus towards WRT is not misplaced. The services sector as a whole contributes upwards of 54% to Pakistan’s GDP[1]. WRT, which constitutes just over a third of all economic activity in the services sector, contributes 18% to overall GDP. This number is greater than large-scale manufacturing’s contribution to the economy, and reflects the changing nature of an economy where between 1999-2000 and 2017-18, the share of services sector has increased from 54% to 60% and consequently, the share of the commodity producing sector has declined from 46% to 40%.

Real growth rates for WRT have hovered around the 4% mark for the last two decades, which while not being spectacular, shows consistent expansion. In terms of employment generation, WRT has emerged as a leading sector providing employment in rural and urban areas of the country. About nine million people are employed in this sector, which is about 16% of the total employed labor force. Most importantly, with private consumption recorded as more than 80% of GDP, and showing little signs of abating, it is clear that domestic commerce will retain its primacy within the country’s economy.

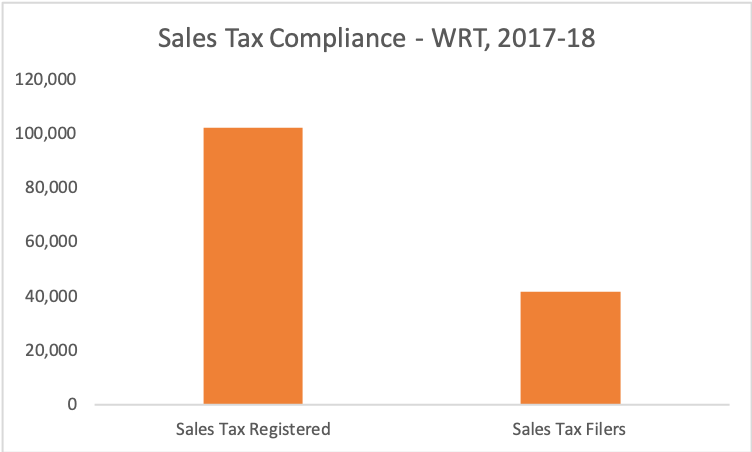

The taxation side of this picture adds further credence to the new budgetary measures proposed for 2019-20. Revenue contribution by WRT is fairly dismal. Historical collection data that is available reveals that during 2006-07 in the heads of both direct and indirect taxes only Rs. 6.8 billion were collected from the sector and there was a nominal increase of 8% in collection till 2009-10.[2] As a whole, the WRT sector contributes around 0.5% in total federal taxes, despite contributing 18% to overall GDP; in terms of compliance it does no better, with only 41% of all Sales Tax NTN holders within WRT (roughly 42,000), and under 60% of all Income Tax NTN holders, who draw their primary income from WRT, filing their sales and income tax returns respectively.

The taxation side of this picture adds further credence to the new budgetary measures proposed for 2019-20. Revenue contribution by WRT is fairly dismal. Historical collection data that is available reveals that during 2006-07 in the heads of both direct and indirect taxes only Rs. 6.8 billion were collected from the sector and there was a nominal increase of 8% in collection till 2009-10.[2] As a whole, the WRT sector contributes around 0.5% in total federal taxes, despite contributing 18% to overall GDP; in terms of compliance it does no better, with only 41% of all Sales Tax NTN holders within WRT (roughly 42,000), and under 60% of all Income Tax NTN holders, who draw their primary income from WRT, filing their sales and income tax returns respectively.

These numbers have received a great deal of political attention as well, with the erstwhile Minister of Revenue, Hammad Azhar, tweeting evidence of paltry figures of total tax collection in major commercial centres of Lahore.

What are the new measures?

In light of its persisting fiscal constraint, the government has introduced a number of new measures in the Finance Act to improve both the visibility of activity and scale of collection. The overriding goal, as repeatedly asserted by FBR chairperson Shabbar Zaidi, is to arrive at a more accurate measure of sales and, consequently, the income being generated through WRT, especially at the retail stage.

Expanding the definition of those liable to register for sales tax

This means that the category of who is liable to register themselves for Sales Tax[3] (and, as a result, deposit it), and file monthly Sales Tax returns, has been expanded to include the covered area (not size/raqba) of the retail location as well (1,000 sq feet and more). This is in addition to existing criteria, such as being part of a national/international chain of retailers, or having a permanent brick-and-mortar shop in an air-conditioned mall, or consuming cumulative electricity of more than Rs. 600,000 per year, or operating as a wholesaler-cum-retailer, engaged in bulk import and supply of consumer goods on wholesale basis to retailers as well as on a retail basis to the general body of the consumers.

Purchasers’ CNIC/NTN on purchases larger than Rs. 50,000

The second change, and the one causing perhaps the greatest amount of consternation, is documentation through the furnishing of the purchaser’s NTN and CNIC on the sales invoice, where the value of good(s) sold exceeds Rs. 50,000. There are several aspects of this provision which have proven to be contentious. The first is the scale of its application – does it cover all retailers, or just Tier-1 retailers? Is it applicable to all wholesalers/distributors/importers who carry sales tax registration or does it also include those who do not? Secondly, there are vagaries built into the text of the provision, specifically those pertaining to the retailer’s assessment of who exactly is an end consumer. Third, there are no clear-cut safeguards mentioned in instances where CNIC’s solicited by a retailer/wholesaler turn out to be false. And lastly, there are issues of privacy and culture, for instance, when a consumer happens to be female, and thus uncomfortable sharing her CNIC details.

Introduction of a fixed-tax multi-tiered scheme

The third major change is within the remit of Income Tax on persons engaged in WRT through the introduction of a fixed-tax multi-tiered scheme. The scheme exists solely for non-Tier-1 retailers, and its incidence is based on the size and location of the outlet, as well as the nature of the business. A large number of businesses (distribution, warehousing, professional services etc.) have been excluded from opting for this scheme. Instead it is aimed at smaller enterprises, engaged in the sale of food and beverages (groceries), and smaller retail commodities. The scheme contains provisions for compliance and registration, and includes the submission of simplified returns.

What are the business community’s reservations?

Without prior judgement, the most prominent reservations, as enunciated by representatives of various trader organizations, are worth considering here.

Costs of compliance, especially for small businesses

Their biggest claim so far, especially those put forward by Naeem Mir’s faction of the All Pakistan Anjuman-e-Tajran (which also happens to be the most well-organized apex body out there) is that attempts at documentation raise compliance costs for small businessmen. With greater penalties and threats in place for not gaining sales and income tax registration (and not filing monthly and annual returns), or for furnishing CNIC-carrying sales invoice for each large transaction, businessmen will have to turn to tax consultants on a regular basis. While this may not be an issue for large wholesalers and distributors, it will adversely impact the functioning of small businesses, many of whom are owned and run by individuals with little or no formal education.

The application of uneven and de-contextualised criteria

The second reservation presented is one that has repeatedly cropped up since the introduction of the two-tiered system for retailers nearly five years ago. Trader representatives insist that using arbitrary measures, such as the covered area of a retail location, does not capture the actual nature or health of the business. A popular example given by them is that retailers in the business of selling fodder often require a large covered area but the value of goods sold is quite low. Hence imposing a sales tax registration condition, and introducing a heavily contingent fixed income tax scheme, and then forcing high compliance costs (which includes new cash registers and regular reporting) on them is an unnecessary burden that will either incentivize evasion or kill businesses.

Double taxation

The third reservation relates to the imposition of sales tax compliance through the sales tax registration system when commercial enterprises are already paying sales tax (at variable rates) through their electricity bills. While FBR representatives cite the sales tax filing figure at 42,000 WRT businesses, to show low-levels of compliance, trader representatives argue that 3.1 million commercial electricity connection holders are already paying sales tax, which is a fact overlooked by the revenue body.

Potential for abuse of powers by officials

The final reservation worth considering relates to the powers granted to FBR, both in terms of the steps it can take to audit businesses, as well as the more informal controls and authority field-level offices exercise on economic activity. The major takeaway here is that increased documentation will lead to greater predation, as lower staff at the FBR remains highly prone to rent-seeking activity.

Is there a way out?

A few considerations raised by the business community are worth considering, even if one can plausibly relate intentions behind them as a way of perpetuating the advantages that are accrued with informality and lack of documentation.

At the same time, the numbers stated in an earlier section show that WRT is not picking up its fair share of the government’s revenue base, which leaves the latter with no option but to pursue greater attempts at documentation.

There is little doubt that this is the most aggressive push at reforming the tax regime around WRT since the 1990s. There is also little doubt that many of the reforms suggested (leaving their scale to one side) here are integral to fixing structural issues with Pakistan’s fiscal condition. Having an actual, in-spirit implemented GST is hypothesized to reduce prices in the long-run and make business processes smoother. Simultaneously, greater visibility of incomes may help the government institute an actually progressive income tax regime, which would reduce burden on white and blue-collar salaried individuals in the formal sector.

Contention is inevitable when status-quo transformations are instituted, especially in areas that relate to economic activity. Broadly speaking, there are two inter-related suggestions worth considering here that may make the political aspects of tax reform slightly easier.

Softening the blow by staggering the reforms

The first is that such an aggressive push needs to be re-considered given that it is taking place at a time when the country is going through a purposeful period of demand contraction. With businesses already experiencing slowdown, and consumers experiencing higher inflation and employment concerns, forcing greater compliance costs and punitive actions on one of the largest segments of the economy is ill-advised. A way out would have been to phase in the interventions over this three-year stabilization period, with sales tax registration remaining the focus in Year One, an expanded and revised fixed income tax scheme, which would include medium and small-sized retailers, being introduced in Year One or Year Two, and the provision of incentives (rather than penalties) for moving towards digital payments and greater transparency in documentation in Year Three.

Greater consultations to generate wider ownership

The second suggestion relates to the processes through which reforms are conceived and pushed through, which is what lies at the heart of the contention in the first place. The amendments introduced and the schemes and procedures associated with them have not been the product of any deliberation between the revenue body and the WRT community. Moreover, the role of parliament is completely absent in a domain (revenue collection) which is one of the foundational logics of the modern state. To this date, a full month after the passage of the Finance Act, it is unclear what the role of the finance committee has been, what elected representatives have contributed (or been allowed to contribute) towards these issues.

Deliberation and transparency in any reform process is necessary for increased buy-in and to minimize opposition. To date, the government has shied away from opening up complex issues of fiscal management to a larger section of stakeholders, preferring to come up with solutions behind closed, highly bureaucratic or technocratic, doors. But these are issues, by very definition, that have a political character. The conflict with the trader community is a symptom of the larger malaise of an apolitical process to achieve essentially political aims, i.e. greater fiscal strength for the republic. Any government that seeks to validate its pro-reform credentials would have to transform the very nature of how such crucial decision-making is carried out.

References

[1] Economic Survey of Pakistan (2017-18)

[2] Industry Profile: “Wholesale and Retail Trade Sector in Pakistan”, FBR Quarterly Review Vol 12, No. 2, Oct-December 2012

[3] Tier-1 retailers under clause 43 of the Sales Tax Act

4 Cover image: Reuters

Assistant Professor of Politics and Sociology at the Lahore University of Management Sciences (LUMS), and a Non-Resident Fellow for Political Economy at Tabadlab.