Summary

• Around 100 million adults in Pakistan are unbanked – they don’t use formal and regulated financial services. This means that more than 50% Pakistanis do not have a financial and credit history, making them ineligible for access to credit through commercial banks.

• Microfinance banks and institutions offer products and services to clientele that does not get served by commercial banks, but their penetration is limited, and their financial products and services are very costly.

• Digital Financial Services (DFS) are an alternative financial solution, providing access to quick credit, loans and micro/nano investment opportunities for the economically vulnerable and financially undocumented.

• Despite Pakistan’s active DFS ecosystem and significant progress, there is limited adoption in Pakistan resulting in over 70% of the population being financially excluded.

• Policymakers should create supporting policies to catalyse the growth of DFS to create value and necessitate a behavioural shift towards digital financial services.

• For the Ehsaas Emergency Cash program, the Government can leverage service providers to achieve a more efficient and safe process by disbursing cash transfers to mobile accounts/wallets.

• Policymakers should factor in women-specific needs into design and outreach plans of digital financial services.

Identifying the Problem

Globally, countries have adopted innovative methods and transformative approaches to manage the shockwaves generated by the uncertain nature and lifespan of the COVID-19 pandemic. Depressed economic conditions amplified due to the pandemic have sparked intense debates about the social contract, safety nets and the role of the state in supporting welfare programmes for the economically vulnerable.

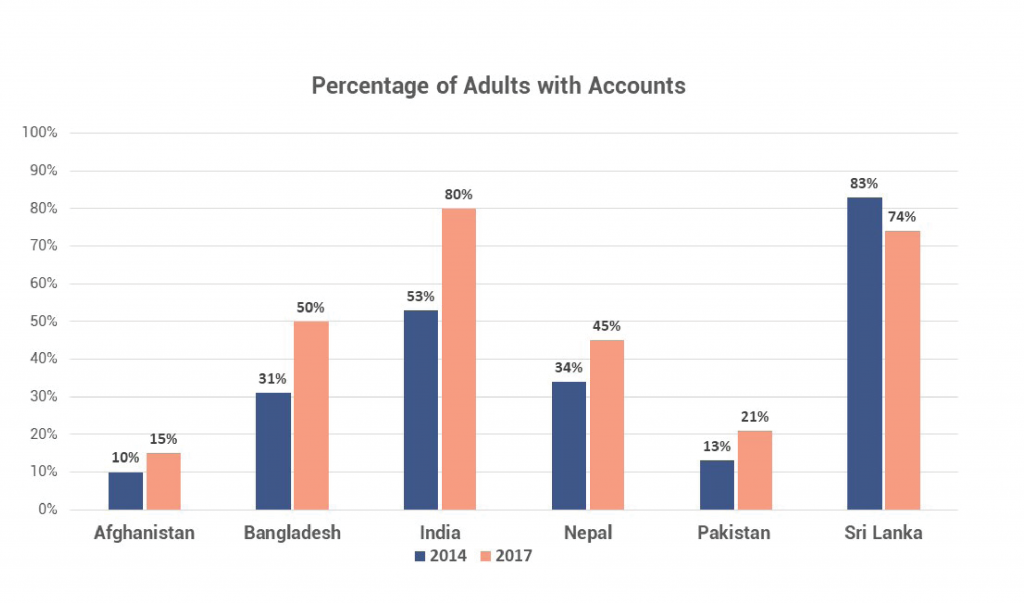

with accounts in South Asia

An elaborate welfare programme by the Government of Pakistan was introduced to mitigate economic shocks during the pandemic. The Ehsaas Emergency Cash program has catered to 15 million vulnerable households, covering nearly half of Pakistan’s population . However, the impact of the pandemic is wide-reaching and an economy with weak fundamentals and a dampened growth trajectory can only support state-driven welfare to a limited extent. This will necessitate the need for markets to function and devise clearing mechanisms to respond to societal demands for financial products and services beyond what the state covers.

Two key issues impede a well-regulated and functioning financial services sector in Pakistan:

- A large informal and undocumented economy contributing approximately 35% to the GDP and employing 70% of the workforce.

- The limited penetration of financial services to ensure transactions are documented, and individuals and business can access financial products during financial distress.

Pakistan’s economic activity is classified as informal, where most transactions are settled in cash and do not get documented. Around 100 million adults in Pakistan don’t use formal and regulated financial services . This means that more than 50% Pakistanis do not have a financial and credit history thereby making them ineligible for access to credit through commercial banks. Microfinance banks and institutions do bridge some of this gap by offering products and services to clientele that does not get served by commercial banks but their penetration is still limited, and financial products costly.

Digital Financial Services (DFS) are an alternative to physical transactions and person-to-person contact. This makes them an essential component of containment measures adopted as a pandemic response, especially in the case of smart and/or micro lockdowns. Additionally, economic resilience and recovery can be strengthened by a financial system that is capable of responding to unique and unconventional needs. Quick credit, loans and micro/nano investment opportunities can be provided to economically vulnerable individuals and businesses being pushed further down by the economic conditions during the pandemic. Despite Pakistan’s active DFS ecosystem and significant progress, these alternatives to conventional fi-nancial services still have limited adoption in Pakistan resulting in over 70% of the population being financially excluded. Moreover, while there are around 50 million mobile wallets, less than 10% are active.

Why does this problem exist?

Informal economics occupies a central role in the lives of the poor. Economically vulnerable groups rely on unregulated work and informal financial relationships in order to manage risks, sustain livelihoods, and build safety nets e.g. saving and borrowing, are managed through informal financial structures at a family and community level. Informal financial relationships are preferred due to easy and quick access, and no paperwork requirements. However, while these relationships are viable temporary solutions, they are unreliable and can’t be used as a sustainable means to varying financial needs of households.

In Pakistan, a number of factors have hindered a shift towards DFS:

The absence of a coherent digitalization vision and strategy for the country’s economy. Pakistani policymakers have not conceived of the impact of digital transformation on society, economics or politics. Resultantly, digitalization has been lead by the private sector, and state interventions have been reactive, rather than proactive. Some would argue that the last major digitalization reform that served citizens at scale was the adoption of Calling Party Pays (CPP) regime that enabled low income groups to use mobile phone viably. That reform was almost two decades ago.

Cost of providing DFS at scale limits accessibility and success. 90% of the Pakistan’s population is registered through NADRA and offers a massive scale to use the biometric verification as a digital asset . DFS providers are required to validate identity and fulfil Know Your Customer (KYC) compliance protocols. The cost of verifying users and transactions at scale (largely for new accounts and over the counter trans-actions repeatedly) makes the business model less viable for DFS providers, particularly new entrants and small-scale operations.

Reluctance to use financial services as a means for documentation and taxation. Undocumented income sources and informal financial relationships help individuals and businesses to avoid the tax net. The use of DFS, despite its wide-ranging advantages, will result in documentation of the economy and hence has been resisted by large segments of the country to retain and grow tax-free earnings.

User behaviour, attitudes and experience have not been a priority. The DFS landscape in Pakistan is heavily focused on digital payments as opposed to other use-cases like saving, investment and lending. For holistic financial inclusion, the market needs to cater to all use-cases. As an example, in order to increase lending, a credit scoring system has to be formulated to assess the worthiness of an individual in absence of collateral. This could be done through alternative data points like smart phone data, utility bills data and commercial purchases. The unavailability of this data and its linkages to creating an alternative credit scoring mechanism is attributable to a weak enabling environment to increase adoption of DFS for everyday use-cases. In most countries, this agenda is driven by the government, supplemented by industry stimulating tax incentives and consumer-protecting policies.

Importance and Implications

Financial exclusion affects economic wellbeing. In order to cope with the economic pressure of COVID-19 and a slump in economic activity, individuals and businesses both require a cushion to bridge financial needs. This can be done by accessing quick and flexible credit. Since conventional banks lend to the clients with a robust credit history (formal economy participants), unbanked individuals and the economically vulnerable are excluded from these financial services. DFS providers can offer alternative means to provide rapid services with potentially lower costs and tailored approaches in such circumstances. Having no access to market-driven financial solutions increases the pressure on the limited resources of the state and a dilution of support available to most vulnerable groups.

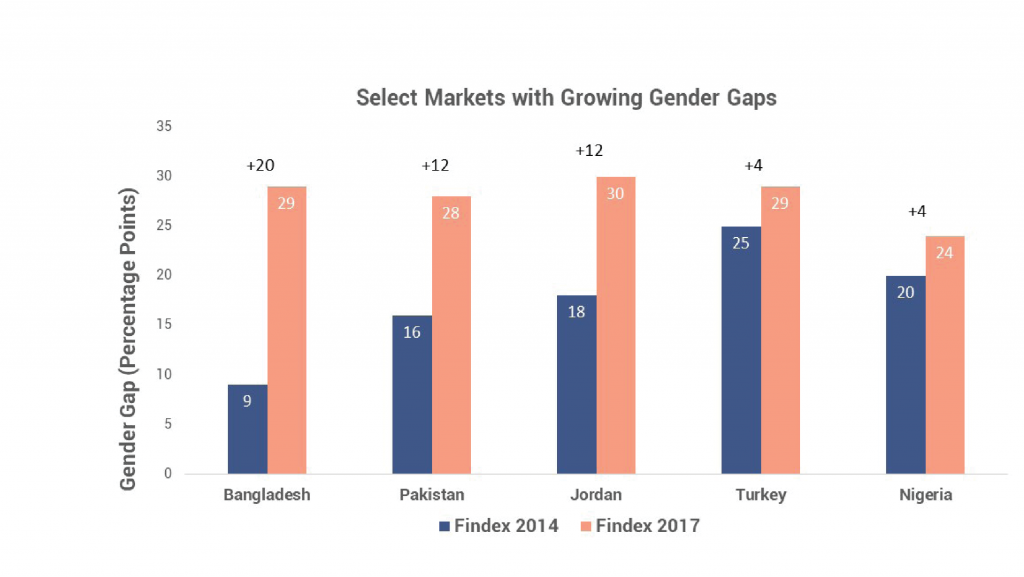

Females are more exposed to economic vulnerability in comparison to males. Due to cultural attitudes towards women’s education and employment, women are more likely to be a part of low paid, unskilled workforce which is devoid of adequate labour regulations.

The economic constraints that have emerged during this pandemic have resulted in loss of jobs and wage reductions for female workers engaged in activities like cottage industries and domestic help. In addition to their existing financial vulnerability, women also often lack control over their own money Great autonomy over household financial decisions for women has proven to benefit education, health and wider welfare outcomes.

Public and private sector response programmes can be enhanced significantly through integration of DFS. Use of digital tools and aids in response interventions can increase scale, efficiency and transparency. The use of DFS as a mainstream transaction channel by government can enable a faster uptake of such services across segments interacting with systems and receiving such payments.

In the case of the Ehsaas Emergency Cash program, the Government could have leveraged service providers to achieve a more efficient and safe process by disbursing cash transfers to mobile accounts/wallets rather than restricting to only two banks and their agents. Individuals were still required to visit campsites and banks to collect cash disbursements which presented its own set of problems in terms of safety during a pandemic and for women, the elderly, disabled, and those coming from a distance with little financial resources.

Recommendations

1

Rationalisation of Costs

There should be a removal of, or reduction in, NADRA’s fees for identity verification in order to provide an opportunity for DFS providers to develop a viable business model that is scalable. This would also lead to a reduction in the cost base resulting in provision of affordable services for consumers, and making DFS more accessible and inclusive.

2

‘Open Banking’ Model

An ‘Open Banking’ model should be adopted whereby third party financial service providers have open access to financial data from banks and non-bank financial institutions. Telcos and banks should be repositories of data as opposed to owners. Data on customers should be made available to third parties with customer consent in order to ensure that a large proportion of Pakistanis are included in the system.

3

Alternative Credit Scoring System

To provide economic relief to low income consumers, NADRA, the State Bank of Pakistan, and FinTech companies should collaborate to create a credit scoring system to assess the credit worthiness of an individual. This could then be used to build a risk profile of borrowers to assess their repayment capability. Since low-income individuals and small businesses are less likely to have assets, and a robust financial history to support a case for a loan, FinTechs could bridge this gap by creating a risk profile through the credit scoring system. This would ensure financial inclusion in general, and relief during this pandemic.

4

Increased use of DFS by the public sector

The Ehsaas Emergency Cash program should be a model large-scale initiative adopting a digital first strategy. It already uses a robust data regime to identify individuals eligible for cash disbursements; the same data could be used to integrate digital transfers through mobile wallets. A government push could help familiarise individuals with digital financial services, which could trigger a behavioural shift and help consumers adopt these DFS for regular use. Other use cases for government include the payment of government salaries through DFS, especially for those in BPS 1-16, a cohort that likely serves as a vital community of first-in users of new ways of doing things across the country.

5

Gender Focused Solutions

Specific needs of females should be factored into product design and outreach plans of digital financial services. This should be supported by research and insights that unpack challenges and barriers for improving access for women e.g. mobility constraints, literacy and access to digital technologies. Gender disaggregated data should be formulated to support evidence-based decisions.

6

Digital and Financial Literacy

If the use of digital financial services is to reach those at the bottom of the pyramid, digital literacy must be improved on a fast-track and should be incorporated at multiple layers in the formal, informal, skills and other education streams. To participate in the digital economy, policymakers need to draw attention towards promoting digital and financial literacy and also formulating special programs for vulnerable groups like women, the elderly, differently abled and micro, small and medium enterprises.

This material has been developed by Tabadlab in partnership with DRI. It has been funded by UK aid from the UK government; however, the views expressed do not necessarily reflect the UK government’s official policies.

Sources

- APP, ‘Ehsaas Emergency Cash Program: an Extensive Social Protection Intervention’. Daily Times, Nov 12, 2020.

https://dailytimes.com.pk/688068/ehsaas-emergency-cash-program-an-extensive-social-protection-intervention/ - Fahad K. Niazi, ‘Policy and Regulatory Bottlenecks for Digital Financial Services in Pakistan’. Karandaaz, May 2019.

- Financier Worldwide Magazine, ‘Role of FinTech in the Post-COVID 19 World’. Nov 2020.

- Francois Bonnet and Sudhir Venkatesh, ‘Poverty and Informal Economies’, in David Brady and Linda Burton (dir.), Oxford Handbook of the Social Science of Poverty, Oxford University Press, pp. 637-659.

- Gallup, ‘Findev Cyberletter’. 23rd Edition.

- Genesis Analytics, ‘Exploring Fintech Solutions for Women’. IDRC, Mastercard Lab, 2018.

- Laura Brodsky and Liz Oakes, ‘Data Sharing and Open Banking’. McKinsey and Company, Sep 5, 2017.

- Lubna Razaq, ‘Making Digital Lending Work’. MIT Technology Review.

- Mayada El-Zhogbi, ‘Measuring Women’s Financial Inclusion: The 2017 Findex Story’. CGAP, Apr 30, 2018.

- Nadeem Haque, ‘Microfinance and Fintech’. MIT Technology Review.

- Nguyen V. Khuong, Malik S. Shabbir, Muhammad S. Sial, and Thai H. T. Khanh, ‘Does Informal Economy Impede Economic Growth? Evidence from an Emerging Economy’, Journal of Sustainable Finance and Investment, Jan 9, 2020.

- NNI, ’70 pc of Pakistan’s Economy is Informal, which is of High Concern: PBI’. The Nation, Feb 6, 2019.

- Robert Cull, Tilman Ehrbeck, and Nina Holle, ‘Financial Inclusion and Development: Recent Impact Evidence’. World Bank, CGAP, No. 92, Apr 2014.

- Samia Salik, ‘The Impact of Biometric Verification Systems on Financial Inclusion in Pakistan’. Karandaaz, Jan 2020.

- Stephen Rasmussen, ‘Pakistan Enigma: Why is Financial Inclusion Happening so Slowly?’. CGAP, Oct 30, 2018.

- Tabadlab, ‘Building Pakistan’s Fintech Ecosystem’. Pakistonomy, Ep 40.

- Mosharraf Zaidi and Umar Nadeem, ‘Analysis of the COVID-19 Ehsaas Emergency Cash Income Support’. Tabadlab, First Response, Mar 30, 2020.

- TR Pakistan, ‘Creditfix Approving Borrowers Lenders Missed’. MIT Technology Review, Jun 7, 2017.