Insights from the Global Findex 2021

Covid-19 has accelerated digital transformation globally, leaving a particularly prominent impact on the global financial sector. Today, more people aged 15+ hold an account than ever before and the gender gap has contracted.

Adult account ownership in developing economies increased to 71% in 2021 (from 63% in 2017). Meanwhile, the average gender gap is now 6 percentage points, down from 8 percentage points in 2017. However, some countries continue to lag across both indicators.

Topline financial inclusion remains stagnant

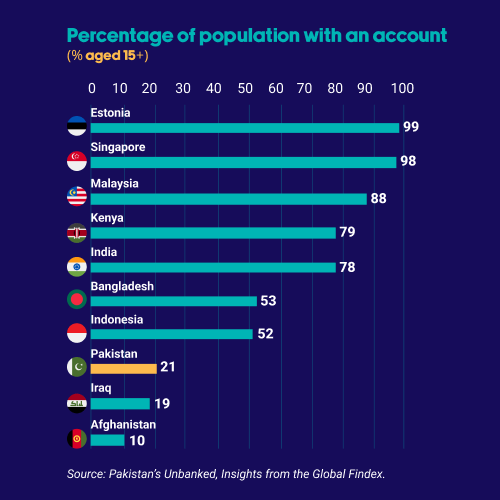

Pakistan houses 2.8% of the world’s population, but 8% of the world’s unbanked adults. This imbalance is reflected in the country’s low topline financial inclusion indicator, which appears to have stagnated at 21% between 2017 and 2021.

The topline demand-side financial inclusion indicator has not changed despite several market developments in the 2017-2021 period. This includes the introduction of new regulations, market infrastructure (Raast), players (fintechs), and pricing structures (zero-cost IBFT < PKR 25K).

In absolute terms, the total financially included population has in fact increased slightly from 28 million to 31 million from 2017-21. Pakistan’s population growth masks this small improvement. Despite this marginal increase, Pakistan’s performance on the Findex is concerning, especially in comparison to peer countries.

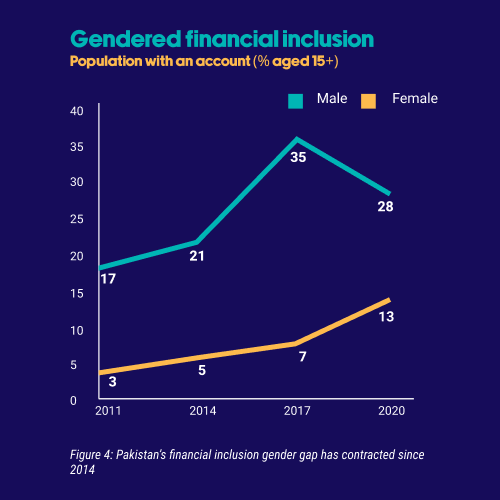

Female account ownership has almost doubled

A deeper look at the Findex reveals an odd phenomenon: some people have fallen out of the formal financial net, while others have simultaneously entered. This is particularly evident when we look at the narrowing gender gap. The gap has decreased as a result of more women becoming financially included, and more men becoming financially excluded.

Between 2017 and 2021, women’s account ownership almost doubled, while men’s account ownership declined by 7 percentage points.

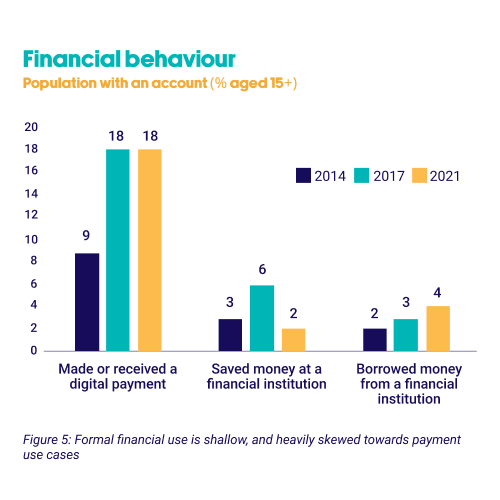

Adoption of financial services remains shallow

The shifts revealed in the Findex are indicative of a simple truth: for the vast majority of people in Pakistan financial inclusion tends to be extremely shallow and thus vulnerable to external shocks. Tellingly, relatively more adults report having made or received a digital payment, but many do not, or cannot, access formal savings or credit solutions. Interestingly, in 2017-21, the number of women using digital payments more than doubled (from 5% to 11%). This is in line with the growth in female account ownership and indicates a link between digital payments and financial inclusion.

Impediments to account ownership

Certain characteristics increase an individual’s likelihood of being financially included. Those who were unbanked most commonly cited three primary reasons for staying out of the formal financial net, as captured in Figure 7.

Given that insufficient funds is the biggest contributing factor to exclusion, it is worrying that 62% of people reported experiencing financial difficulties due to Covid-19.

Relatedly, more than 4 out of 5 unbanked adults said that they could not use a financial institution account without help. This indicates that discomfort with formal financial services and insufficient support could both be barriers to entry.

Digital payments offer a gateway to financial inclusion

- Globally, digital payments have acted as a gateway to financial inclusion. In Pakistan, where 55% of unbanked Pakistanis aged 15+ have a mobile phone, mobile-based digital payments have the potential to unlock the broader digital economy.

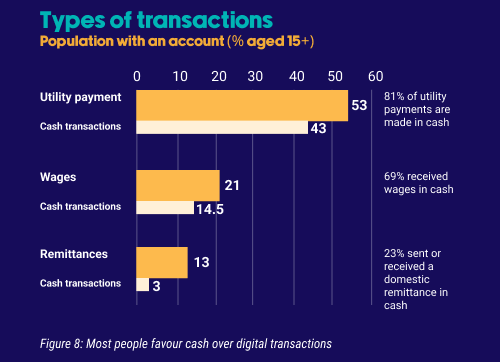

- The Findex provides insights into the type of transactions that people are engaged in, and indicates preference for cash.

Based on the transaction data captured in the Findex, high potential areas for payment digitisation include:

- Utility bills: While more than half the adult population pays utility bills, over 80% do so in cash, representing a huge target segment for financial service providers.

- Private sector wages: Digitising private sector wage payments could bring around 20 million unbanked adults into the formal financial system.

- Domestic remittances: Targeting this use case could unlock value for this 4 million person strong segment.

Naeha Rashid

Naeha was formerly Senior Manager at the Centre for Digital Transformation. She is passionate about the potential of technology solutions to improve the quality and character of people’s lives. Naeha has previously worked with a variety of organisations including Harvard's Ash Center, CGAP (a member of the World Bank Group), and Karandaaz Pakistan to catalyse digital innovation and enhance inclusion both in Pakistan and abroad. She has an MPP from Harvard University, and a BA (Hons) in International Development and Economics from McGill University.